What Is the IMMEX Program?

The IMMEX program (Industria Manufacturera, Maquiladora y de Servicios de Exportación) is a Mexican government program that allows manufacturers to temporarily import raw materials, components, and fixed assets — machinery and equipment — into Mexico without paying general import duties, provided the goods are used in production for export. It is the legal framework behind most maquiladora operations, and it is the reason a US parent can equip a Mexican plant with foreign machinery without treating every machine as a definitive, duty-paid import.

Whether you are evaluating the IMMEX program Mexico offers as part of a nearshoring move or already manufacture under IMMEX in Mexico, the benefit comes with a standing obligation that many US controllers only discover when Mexico's tax authority (SAT) starts asking questions: every temporarily imported good — including every machine on the floor — must be tracked, per import document, in an automated inventory-control system whose minimum content is defined by Anexo 24 of the General Foreign Trade Rules. This guide covers both halves: what IMMEX requires to get in, and what Anexo 24 requires to stay in — with particular depth on the part nearly every English-language guide skips, the mandatory fixed-asset (Activo Fijo) module and the physical verification that stands behind it.

IMMEX Requirements, Qualification and Certification

IMMEX authorization is granted by Mexico's Ministry of Economy (Secretaría de Economía) to a Mexican-resident legal entity. A US company cannot hold an IMMEX program directly: it either incorporates a Mexican subsidiary or manufactures under a shelter operator's program. The core qualification requirements are structural rather than exotic:

- A Mexican corporation with federal tax registration (RFC) and a tax-compliant standing;

- An export commitment — maintaining the export-sales levels the IMMEX Decree requires;

- Registered operating domiciles — every plant and warehouse where temporarily imported goods will be located must be listed in the program authorization;

- An Anexo 24-compliant automated inventory-control system, available to the customs authority, from the first temporary import onward.

Processing timelines for a complete application vary; the practical timeline is set by the prerequisites — incorporation, tax registrations, domicile registration, and standing up the inventory system. Separate from the IMMEX authorization itself, many companies also pursue IVA/IEPS certification (commonly referenced as RECE/CIVA), which grants a credit against the VAT that would otherwise apply to temporary imports. That certification adds its own obligations — including the Anexo 30 account system covered later in this guide — and it is one of the first things SAT can suspend when inventory controls fail.

What Is Anexo 24 (Annex 24)?

Anexo 24 is an annex to Mexico's General Foreign Trade Rules (Reglas Generales de Comercio Exterior, RGCE) titled "Sistema automatizado de control de inventarios" — the automated inventory-control system. It defines the minimum information an IMMEX company's customs inventory-control system must contain. Three points matter for a US reader:

First, the legal chain is explicit. Article 59, section I of the Ley Aduanera (Customs Law) obligates importers to keep automated inventory control; Article 24, section IX of the IMMEX Decree applies that obligation to IMMEX holders; and RGCE rule 4.3.1 ties IMMEX companies specifically to the catalogs and modules of Anexo 24, Apartado I. Second, Anexo 24 is a data standard, not a software product — companies may run any platform that meets the specification, but an Excel workbook or a standalone fixed-asset list does not satisfy the "automated system" requirement. Third, the obligation is continuous: the system must be current and available to the customs authority for as long as temporarily imported goods remain in Mexico, which for machinery can mean the entire life of the program.

One disambiguation is worth making early, because it confuses even bilingual teams: Mexico has a different "Anexo 24" in its e-accounting rules under the Miscellaneous Fiscal Resolution. This guide covers the customs Anexo 24 — the RGCE inventory-control standard for foreign-trade operations — which is the one an IMMEX audit runs on.

Anexo 24 System Requirements: Catalogs, Modules and Reports

Anexo 24, Apartado I prescribes a specific architecture. The system must contain three catalogs: the taxpayer catalog (contribuyente — legal name, RFC, IMMEX program number, and every registered plant and warehouse address), a materials catalog, and a products catalog. On top of the catalogs sit four customs modules: entries (entradas), exits (salidas), materials used (materiales utilizados), and fixed assets (Activo Fijo). A reports module must generate, at minimum, reports of entries, exits, balances by tariff code, and materials used — with the company name and RFC on every report.

Two operational rules follow from the standard. Discharges must follow a PEPS (first-in, first-out) method covering both materials and the machinery and equipment imported under the program. And because the system is the company's legal evidence of where every temporarily imported good stands, its balances must be reconcilable to the underlying pedimentos at any time — not reconstructed after the audit notice arrives. Raw-material balances get most of the attention in practice, and the inventory side of the system is its own discipline; CPCON's inventory audit services cover that half. The rest of this guide focuses on the module that gets the least attention and carries some of the largest per-line exposure.

The Fixed-Asset (Activo Fijo) Module — the Part Everyone Skips

The Activo Fijo module is not optional. It is one of the four customs modules Anexo 24 names, and it must carry, for every temporarily imported machine, at minimum: a description including brand and model, the pedimento number (composed of the customs office and dispatch section, the broker's patente, and the document number), the pedimento date, and the clave de pedimento — the operation key that says what kind of import it was. Some system implementations also carry the purchase-order number.

Just as important, the module must record every movement in the asset's customs life: imports, exports, returns, transfers between IMMEX companies, donations, destructions, and regime changes. A machine that was virtually transferred to a sister plant, or scrapped, or converted to a definitive import, must show that event in the module with its supporting pedimento. Serial number and plant location are not strictly mandated by Anexo 24 — but they are near-universal best practice, because without them the record cannot be matched to a physical machine during an audit, which defeats the module's purpose. An Activo Fijo record that cannot be physically located is, in every sense that matters, a ghost asset — with customs liability attached.

Why does everyone skip it? Because the module has no daily transaction volume. Materials flow in and out every day and force attention; machinery enters once and sits for years. The module quietly drifts away from the floor — machines move, get cannibalized for parts, get scrapped without an exit pedimento — until the authority selects five assets and asks for proof.

Pedimento in English: A Glossary for US-Based Teams

A pedimento is Mexico's official customs entry declaration — the legal document that proves goods entered or left the country lawfully. For a US controller reading Anexo 24 exports, the vocabulary that matters most is the clave (pedimento key) taxonomy, because the key determines the legal regime the asset sits under:

| Term / Key | What It Means |

|---|---|

| AF | Temporary import of fixed assets under IMMEX (replaced the historical H3 and A6 keys). The key most plant machinery should carry. |

| A1 | Definitive import — duty paid, not controlled under Anexo 24. A machine on A1 is legally "domestic." |

| RT | Return (retorno) of temporarily imported goods abroad — the exit document that discharges the temporary import. |

| V1 / V5 | Virtual pedimentos — paired documents recording a transfer between IMMEX companies without the goods physically crossing the border. |

| F5 | Change of regime from temporary to definitive import — one of the main regularization routes for machinery staying in Mexico. |

| BO | Temporary export for repair or substitution (Art. 117 Ley Aduanera) — how a machine legally leaves for service and comes back. |

| A3 | Regularization pedimento — the vehicle for legalizing goods with no pedimento or expired temporality (Art. 101 Ley Aduanera). |

| Descargo / legal estancia | Descargo is the discharge of a temporary import against an exit event. Legal estancia is lawful presence — provable, per Art. 146 Ley Aduanera, only by customs documents, authorized-authority documents, or qualifying CFDI invoices. |

The taxonomy is not trivia. In the field, a machine recorded under the wrong key — an AF that should be IN, a definitive A1 sitting in the Activo Fijo module, an unmatched V1/V5 pair between sister plants — is one of the most common audit findings, and each has a different fix.

How Long Can Assets Stay? 18 Months vs. Program Life

IMMEX permanence periods differ sharply by category, and conflating them is a classic US-side misunderstanding. Raw materials and components imported temporarily must generally be returned or discharged within 18 months. Fixed assets are different: machinery and equipment imported under key AF may remain in Mexico for the entire validity of the IMMEX program (Art. 108, section III of the Ley Aduanera, with Art. 12 of the IMMEX Decree) — indefinitely, as long as the program stays active.

That generosity has two conditions attached. The asset must be used in the authorized processes of the program, and it must physically remain at the domiciles registered in the IMMEX authorization (Art. 24, section VI of the IMMEX Decree). A perfectly documented machine found at an unregistered warehouse is an audit finding even though every pedimento exists. The practical consequence for multi-site operators: plant-layout and location discipline is a customs control, not just an operations preference, and every relocation needs to end with an updated register.

What SAT Tests in a Visita Domiciliaria

A visita domiciliaria de comercio exterior is an on-site customs audit, and for fixed assets its mechanics are concrete. The auditors select machines — from the floor, or from the Activo Fijo module — and demand, per asset, three things that must match exactly: (1) the physical machine with its serial plate, (2) the Anexo 24 fixed-asset record, and (3) the supporting pedimento and invoice file. The company is expected to produce all three in minutes, not days. Failure produces observations, tax assessments, and in serious cases a precautionary embargo of the goods and a PAMA (Procedimiento Administrativo en Materia Aduanera).

The underlying test is a dual reconciliation, and it runs in both directions. Book-to-floor: every record in the Activo Fijo module must correspond to a machine that can be physically located. Floor-to-book: every foreign-origin machine on the floor must trace to a pedimento and an Anexo 24 record — including rented, loaned, and consignment machines, which need a lease or comodato contract plus the owner's pedimento or CFDI. This is the same discipline as any fixed-asset reconciliation, with a customs ledger in place of the general ledger. Practitioners frame full compliance as reconciling "four worlds": the physical operation, the pedimentos, the Anexo 24 system, and — for IVA/IEPS-certified companies — the Anexo 30 balances. Most companies that fail an IMMEX fixed-asset audit fail it in the gap between world one and the other three, which is why audit preparation for an IMMEX plant starts on the floor, not in the file room.

Penalties: Presumed Definitive Importation, Fines and Program Cancellation

The headline risk is the presunción de importación definitiva. If a company cannot prove the legal temporary importation of an asset — pedimento plus Anexo 24 record — or a permanence period expired without a return or regime change, SAT presumes the good was definitively imported without paying taxes. The assessment then stacks: general import duty, VAT, any countervailing duties, inflation adjustment, surcharges, and fines. For high-value machinery — production lines, industrial robots — a per-asset assessment can reach a material fraction of the machine's value, which is why the exposure is best understood per line of the Activo Fijo module, not as an abstraction.

Failing to keep the Anexo 24 system itself carries fines that have run on the order of MX$20,000–41,000 per violation under the Ley Aduanera — amounts are adjusted periodically, so treat the range as indicative and confirm current figures with counsel. The escalation path costs more than the fine: more frequent and more intense SAT audits, suspension or revocation of IVA/IEPS certification (with the VAT credit that goes with it), loss of OEA status, and ultimately cancellation of the IMMEX program — which converts every temporarily imported good in the building into an immediate customs problem. Set against the ordinary costs of an unmanaged asset base, IMMEX duty-and-fine exposure is an additional bucket with a regulator attached.

2024–2025 Rule Changes: the 48-Hour Rule and SAT's Real-Time Access

Recent modifications to Anexo 24 changed the supervision model in two ways US leadership should internalize. First, companies must register temporary-import and return operations in the system within 48 hours of the operation. Second — and more consequentially — companies must give SAT a user and password for real-time online access to the inventory-control system. The authority no longer waits for an audit to see your balances; it can log in and look.

In parallel, RGCE modifications flagged in 2024 tightened the discharge math for certified companies importing "sensitive" goods (Anexo II of the IMMEX Decree / Anexo 28 RGCE): they must return at least 80% of the value of the previous twelve months' temporary imports, and discharge reports only count when they are valid — pedimentos and keys matching the discharged period. Fixed-asset regime changes and returns feed those calculations, so a sloppy Activo Fijo module now contaminates a metric the authority actively monitors.

The strategic consequence is simple: if SAT can see your book continuously, the only question left is whether your book matches your floor. A discrepancy that used to surface every few years in an audit is now visible, in principle, every day — which converts periodic independent physical verification from good hygiene into the missing control.

Regularization Routes for Non-Compliant Assets

A non-compliant machine is not a dead end — it is a routing decision. Mexican law provides several regularization paths, each fitting a different discrepancy:

- Change of regime to definitive (F5): pay the duties and keep the machine in Mexico permanently — often the rational choice for equipment that will never leave.

- Physical or virtual return (RT / V-keys): discharge the temporary import by sending the asset abroad or transferring it to another IMMEX company.

- Regularization under Art. 101 Ley Aduanera (pedimento A3, RGCE rules 2.5.1 / 2.5.2): the route for assets with no pedimento at all or with expired temporality.

- One-time key rectification (RGCE rule 4.3.10): AF/IN pedimento-key errors can be rectified once — even after SAT has begun exercising audit faculties — subject to a fine under Art. 185, section II.

Choosing among these routes is legal work for the company's customs broker and counsel. What the routes all consume is the same input: a reliable, classified inventory of exactly which machines are non-compliant and in which way. That evidence layer is where the next section comes in.

How to Physically Verify IMMEX Fixed Assets Against Pedimentos

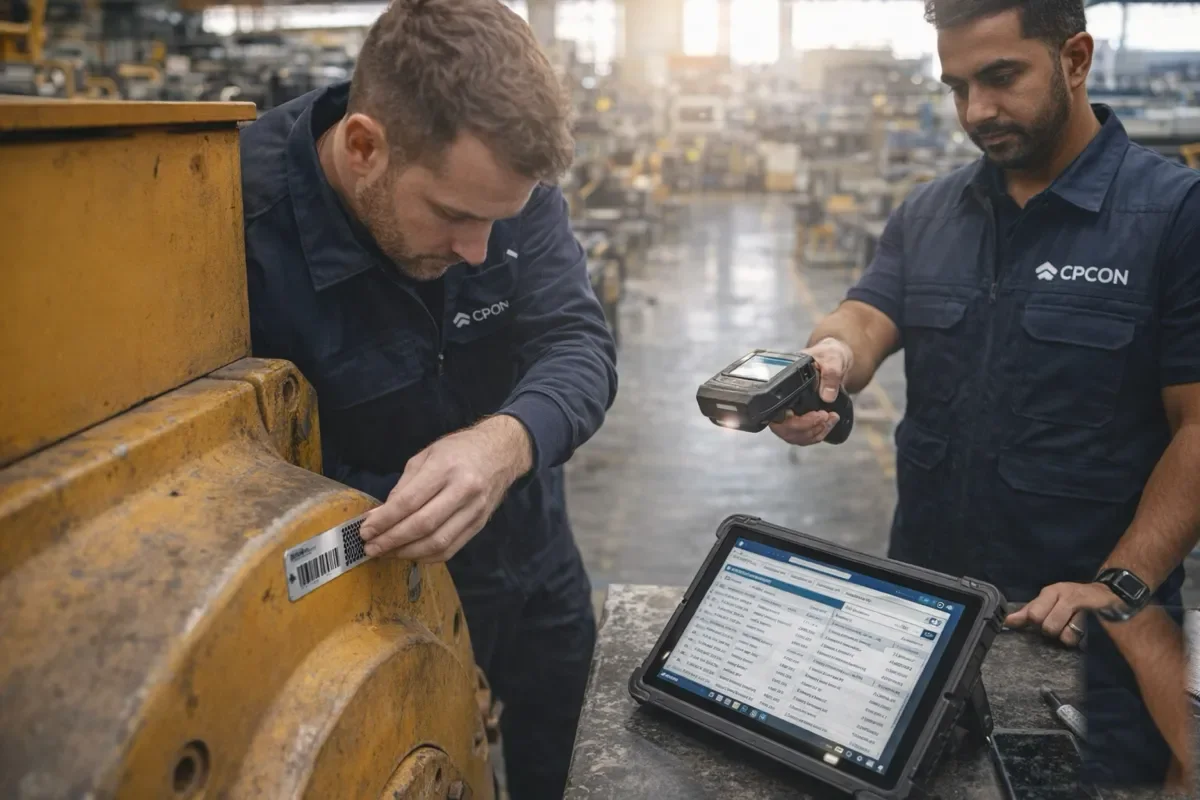

Everything above converges on one operational question: does the machine on the floor match the pedimento in the system? Answering it at plant scale is a fieldwork discipline. CPCON — which has spent 25+ years running fixed-asset inventories for 2,500+ organizations, with Spanish-speaking field crews in Mexico and US-based engagement management — runs it as a five-step methodology:

- Wall-to-wall capture: physically inventory and tag every machine at every registered domicile, recording description, brand, model, serial, and location. The general field method follows the fixed asset verification checklist; the IMMEX layer adds the customs fields.

- Tag design that survives regularization: never encode the pedimento number in the tag itself — a regime change or rectification would force re-tagging the plant. Encode a unique asset ID that links, in the database, to pedimento number, date, clave, serial, and location. (This is standard practice in CPCON's asset tagging work.)

- Dual reconciliation: run book-to-floor using the Anexo 24 Activo Fijo export as the checklist, then floor-to-book tracing every foreign-origin machine to a pedimento. One direction finds ghosts; the other finds undocumented machines. Both matter.

- Per-asset evidence dossier: photograph each asset with its tag, serial plate, and an identifiable plant background; map locations against the authorized IMMEX domiciles. The dossier is what lets staff produce the three-way match in minutes — and mock visita drills are how you find out whether they can.

- Classified discrepancy report: bucket every exception into the taxonomy we see recur in the field — foreign machines with no pedimento on file, ghost Activo Fijo records, expired temporality, mismatched V1/V5 virtual transfers between sister plants, scrapped machines with no exit pedimento, duplicate serials mapped to multiple pedimentos — so broker and counsel can route each to its regularization path.

The deliverable is an import-ready dataset for the client's Anexo 24 Activo Fijo module — asset to pedimento number, date and clave, to serial, to location — plus the classified discrepancy report. One boundary should be stated plainly, because it is both legally accurate and the honest way to buy this service: no consultant can guarantee Anexo 24 or IMMEX compliance. The automated system is a non-delegable obligation of the importer of record. CPCON's role is to feed, cleanse, and evidence that system — independent verification that strengthens the compliance position, performed by a third party that is not selling the shelter or the software. For US parents, the same verified register also feeds the SOX 404 existence assertion on the Mexican subsidiary's PP&E — two compliance regimes, one physical count. CPCON has run engagements of this shape in Mexico for years, including large multi-site operations — see the Prosa Mexico engagement for the in-country delivery model. The engagement itself is scoped as a fixed asset count and tagging project, or as part of a broader fixed asset inventory program with periodic re-verification.

Anexo 24 vs. Anexo 30

The two annexes are frequently conflated because IVA/IEPS-certified companies must maintain both. Anexo 24 is the customs inventory-control standard — catalogs, customs modules including Activo Fijo, and reports — grounded in Art. 59-I of the Ley Aduanera and RGCE rule 4.3.1. Anexo 30 (Annex 30, formerly Anexo 31) is the SCCCYG — the credit-and-guarantee account control system that certified companies use to track the VAT credit on temporary imports, grounded in Art. 28-A of the VAT Law and RGCE rule 7.1.1.

For a fixed-asset audit, Anexo 24 is the primary yardstick: it is where the per-machine records live. But the two systems must tell the same story — a return or regime change recorded in one and missing in the other is itself a finding, which is why the "four worlds" framing treats Anexo 30 alignment as the fourth reconciliation, not an unrelated obligation.

Frequently Asked Questions

What is the IMMEX program?

IMMEX (Industria Manufacturera, Maquiladora y de Servicios de Exportación) is a Mexican government program that lets manufacturers temporarily import raw materials, components, and fixed assets such as machinery and equipment without paying general import duties, provided the goods are used in production for export and tracked in an authorized inventory-control system.

How do I qualify for the IMMEX program — do I need a Mexican corporation?

Yes. IMMEX authorization is granted by Mexico’s Ministry of Economy to a Mexican-resident legal entity, so US parents typically operate through a Mexican subsidiary or a shelter arrangement. Applicants must commit to export thresholds, register their operating addresses, and maintain the Anexo 24 automated inventory-control system from day one.

How long does IMMEX approval take?

Processing timelines vary once a complete file reaches the Ministry of Economy. In practice the timeline is driven by the prerequisites: incorporating the Mexican entity, tax registrations, registering the operating domiciles, and standing up the Anexo 24 inventory-control system that customs obligations assume exists.

What is Anexo 24?

Anexo 24 is an annex to Mexico’s General Foreign Trade Rules (RGCE) that defines the minimum content of the automated inventory-control system every IMMEX company must maintain. It is a data standard, not a software product: three catalogs, four customs modules — including a mandatory fixed-asset module — and required reports.

What does "pedimento" mean in English?

A pedimento is Mexico’s official customs entry declaration — the legal document that proves goods entered or left the country lawfully. Each pedimento carries a number, date, and a clave (key) that identifies the operation type, such as AF for temporary import of fixed assets under IMMEX or A1 for definitive imports.

How long can temporarily imported machinery stay in Mexico under IMMEX?

Raw materials generally must be returned or discharged within 18 months, but fixed assets imported under pedimento key AF may remain for the entire life of the IMMEX program (Art. 108-III Ley Aduanera) — provided they stay in authorized processes at the domiciles registered in the program authorization.

What happens if a machine on the floor cannot be traced to a pedimento?

SAT presumes the good was definitively imported without paying taxes. That triggers import duties, VAT, surcharges, inflation adjustment, and fines, and can escalate to precautionary embargo and a PAMA proceeding. Regularization routes exist — including an A3 pedimento under Art. 101 Ley Aduanera — but they must be executed deliberately.

What is the difference between Anexo 24 and Anexo 30?

Anexo 24 is the customs inventory-control standard for IMMEX companies and includes the fixed-asset module. Anexo 30 is the SCCCYG credit-and-guarantee account system that IVA/IEPS-certified companies use to control deferred VAT. For fixed-asset audits, Anexo 24 is the primary yardstick; certified companies must keep both aligned.